Family Foundations & Tax treatment in the UAE

A correctly structured Family Foundation can be a powerful tool for holding UAE residential property and leasing it without Corporate Tax applying at the level of the Foundation.

Since the introduction of Corporate Tax in the UAE, one of the biggest areas of confusion has been the treatment of real estate investors, whether individuals, families, or institutional investors.

We believe there is a need to bring more clarity to this topic. So we thought of breaking it down into practical, scenario-based case analysis for our readers.

Case 1: What happens if a client buys an asset under a Foundation or similar structure?

A client may hold UAE real estate through a Foundation or similar entity, provided the relevant Land Department permits that structure to hold property ownership in the UAE.

This is an important point because not every international structure can directly own UAE real estate. In practice, structures from jurisdictions such as DIFC, ADGM, and RAK ICC are commonly considered for asset holding, succession planning, estate planning, ring-fencing, and tax treatment.

The purpose of the structure must be clear. It should not be a disguised commercial or trading arrangement. Where the structure is created for family wealth holding, succession planning, and passive asset ownership, it may fall within the intended framework, subject to the applicable conditions.

Case 2: What happens to the rental income from the asset?

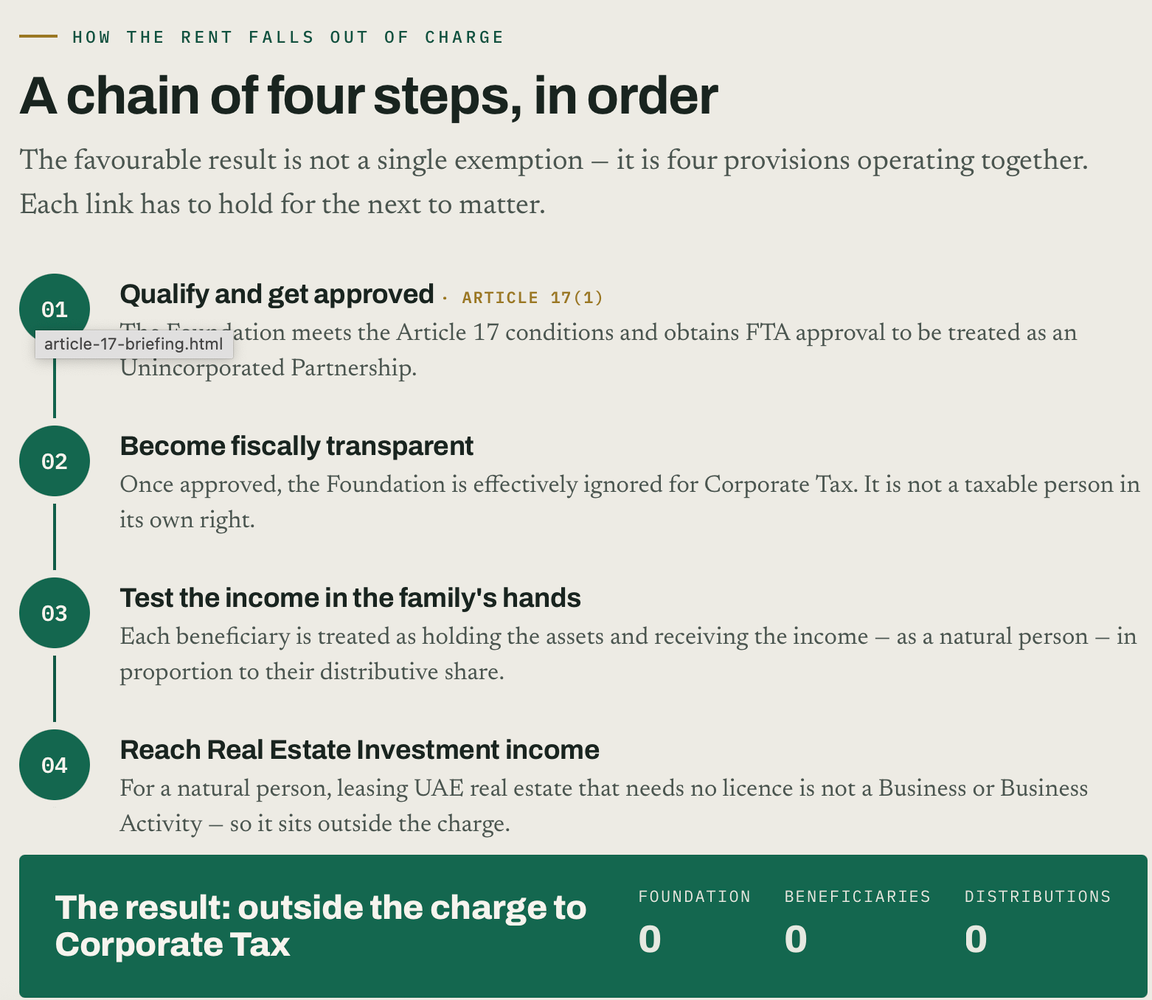

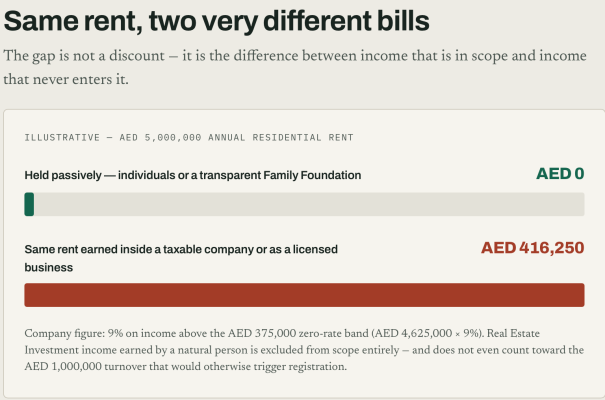

If the property is leased out and the structure has been correctly established, the rental income may not be taxed at the Foundation level because the Foundation may be treated as transparent for Corporate Tax purposes.

The analysis then moves to the beneficiaries/family members. If the rental income is passive real estate investment income of natural persons and is not connected to a licensed business or commercial activity, it may remain outside the scope of UAE Corporate Tax.

This is why the structure matters.

To further explain this,

Case 3: What happens to the tax treatment if the company is sold, or the Foundation structure is changed?

The thumb rule is simple: transparency and passiveness.

First, the UAE does not have a standalone capital gains tax in the way many other jurisdictions do. This has been one of the major reasons for the continued inflow of private wealth, family offices, and investment structures into the UAE.

However, with the introduction of UAE Corporate Tax, the real question is not simply whether there is “capital gains tax”. The real question is whether the gain falls within the scope of 9% Corporate Tax.

This is where Article 17 of the UAE Corporate Tax Law becomes important.

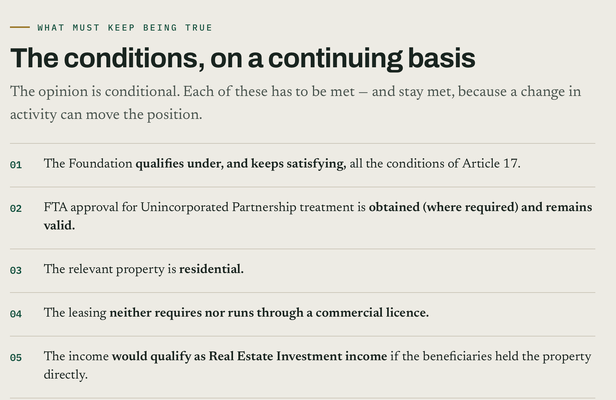

If the Foundation and the underlying structure satisfy the relevant conditions, and the arrangement remains passive in nature, the Foundation may apply to be treated as tax transparent. In that case, the tax analysis may look through the Foundation to the founder or beneficiaries.

Where the underlying gain relates to passive investment or residential real estate investment income of natural persons, and all conditions are satisfied, the 9% Corporate Tax exposure may potentially be avoided.

So the key question is not only:

“Is there capital gains tax in the UAE?”

The better question is:

“Has the structure remained passive and transparent enough to avoid Corporate Tax under the applicable UAE Corporate Tax rules?”

Case 4: What happens if the Foundation sits on top of two SPVs — one passive and one holding a commercial licence?

This is where many structures go wrong.

The test is not always a simple asset-by-asset test. If the Foundation or the structure takes on an activity that would require a licence if carried out directly by an individual, that activity may be treated as a Business Activity. This can potentially disturb the tax-transparent treatment of the entire structure, not only the “offending” asset.

For example:

A Foundation may sit above:

- SPV 1 — holding a passive residential property; and

- SPV 2 — holding a commercial licence or carrying on an active business.

The passive SPV may appear fine on its own. But once the overall structure includes a licensed or commercial activity, the position needs to be reviewed very carefully. The existence of one active business activity can create Corporate Tax consequences for the wider structure and may affect the ability to rely on Article 17 treatment.

This is why the structure must be designed with discipline from the beginning.

A classic trap is holiday homes and short-term rentals.

At first glance, a residential property may look like a passive asset. But if it is used for holiday lets, serviced accommodation, short-stay rentals, hotel-style operations, or property trading, it can quietly cross the line from passive residential leasing into a licensable business activity.

Examples of risky activities include:

- holiday-home permits;

- serviced or short-stay accommodation;

- hotel or motel-style operations;

- frequent buying and selling of properties;

- active property trading;

- commercial leasing or operating activity under a licence.

Once the structure moves from passive ownership to active business activity, the Corporate Tax position can change significantly.So what must investors keep doing?

We at ASK Consultancy specialize in helping you build such efficient and valuable structures in the UAE.

Any Questions?

Connect with lawyers and seek expert legal advice

Share

Find by Article Category

Browse articles by categories

Related Articles

What Most People Don't Know About CBDCs

Imagine waking up one morning to discover that the cash in your wallet has beco…

What Most People Don't Know About CBDCs

Imagine waking up one morning to discover that th…

Accepting Crypto Payments in the UAE: M…

Quick Answer A UAE business cannot simply accept cryptocurrency for its good…

Accepting Crypto Payments in the UAE: Merchant Sa…

Quick Answer A UAE business cannot simply acce…

LEGAL SAFETY RULES — Issue 17 — When …

At the airport, everything moves quickly. A long queue. A sli…

LEGAL SAFETY RULES — Issue 17 — When a Simple F…

At the airport, everything moves quickly. …

LEGAL SAFETY RULES — Issue 18 — AI Ca…

There is a growing trend that many people do not talk about enough. Wh…

LEGAL SAFETY RULES — Issue 18 — AI Can Write. B…

There is a growing trend that many people do not …

One Country, Multiple Court Systems: A …

Ask a newly arrived general counsel to sketch the UAE court system on a whitebo…

One Country, Multiple Court Systems: A Practition…

Ask a newly arrived general counsel to sketch the…

UAE Sets 15 as Minimum Age for Social M…

On 18 June 2026, the UAE Cabinet issued a resolution setting 15 as the minimum …

UAE Sets 15 as Minimum Age for Social Media: What…

On 18 June 2026, the UAE Cabinet issued a resolut…